From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

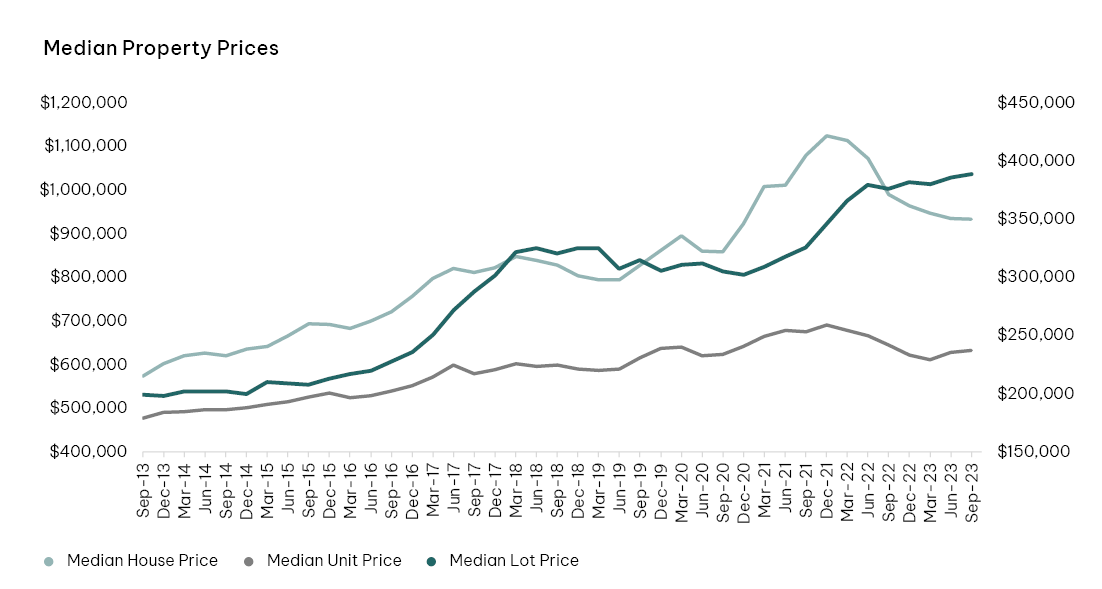

Melbourne’s property market faced challenges in Q3 2023, but potential relief is expected from 2024 to early 2025.

While some factors stabilised in Q3, ongoing challenges (including the future cash rate and inflation) persist. The market continues to adjust to recent cash rate movements which will take time before positive momentum is fully restored.

Market sentiment improved following the stable cash rate in Q3, driven by expectations of reaching the cash rate peak and broader policy stability. However, inflationary pressures led to an additional rate rise in November – this is attributed to local factors rather than global supply chain issues.

While the RBA acknowledges the potential for future rate increases if needed, the broader futures market suggests the cash rate has peaked – pointing to the potential for reduction through H2 2024.

Delivering new supply remains challenging, with elevated (albeit easing) construction costs and high funding costs limiting the feasibility of new projects.

Although easing, the anticipated strong population growth will continue to place pressure on the rental market; maintaining low vacancy rates and firm weekly rents until significant new supply is introduced.

This article references findings from our Q3 2023 Residential Market and Economic Review.