From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

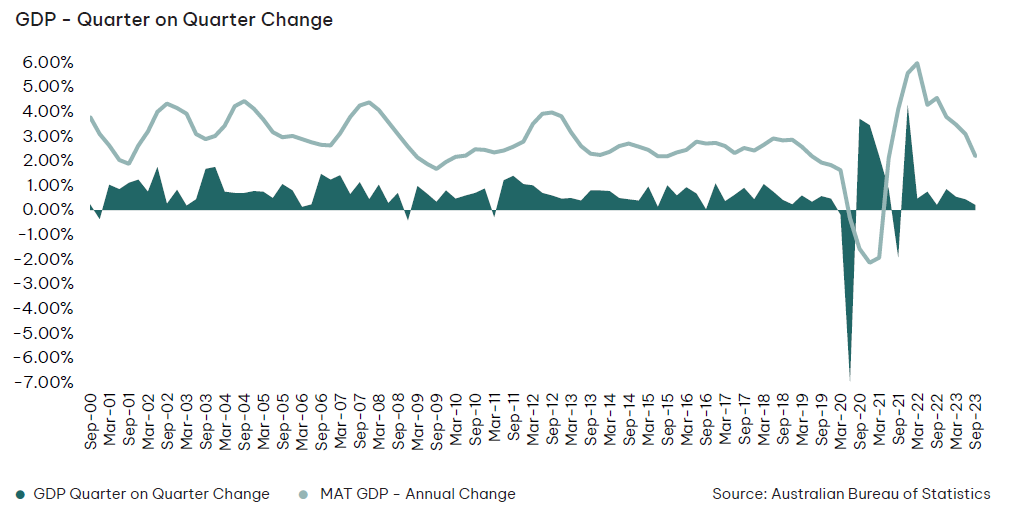

The national economy continued to expand through 2023 however, quarterly GDP growth has slowed as of Q3. GDP per capita is declining as economic growth has not kept pace with the year’s surge in population.

Household consumption remained flat during Q3 2023 as the combination of rapidly rising interest rates and the escalating cost of living pressures continued to take its toll on consumer sentiment. As evidenced by the savings rate dropping to just 1.1%, households are increasingly relying on the savings accumulated during the pandemic to afford essential goods and services.

This challenging affordability and diminishing savings are reducing purchaser activity across the property market; as seen by lower turnover activity in the established market and lower lot sales in the new home market.

Reduced borrowing power and high mortgage repayments are also pushing more would-be purchasers into the rental market, which is already strained by record population growth. As a result, we’re seeing historically low vacancy rates and escalating rental rates.

This supply-demand imbalance is unlikely to alleviate in the short term, given falling building approvals and existing investor stock constituting a relatively higher incidence of on-market dwellings.

Although the cash rate appears to have peaked, the RBA is maintaining a tightening bias as necessary in response to sticky inflation. The need for further cash rate rises in 2024 will largely depend on inflation – which has slowed.

Longer-term property market fundamentals remain sound, however certainty around borrowing capacity will be key to turning around purchaser sentiment.

This article references findings from our Q3 2023 Residential Market and Economic Review.