From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

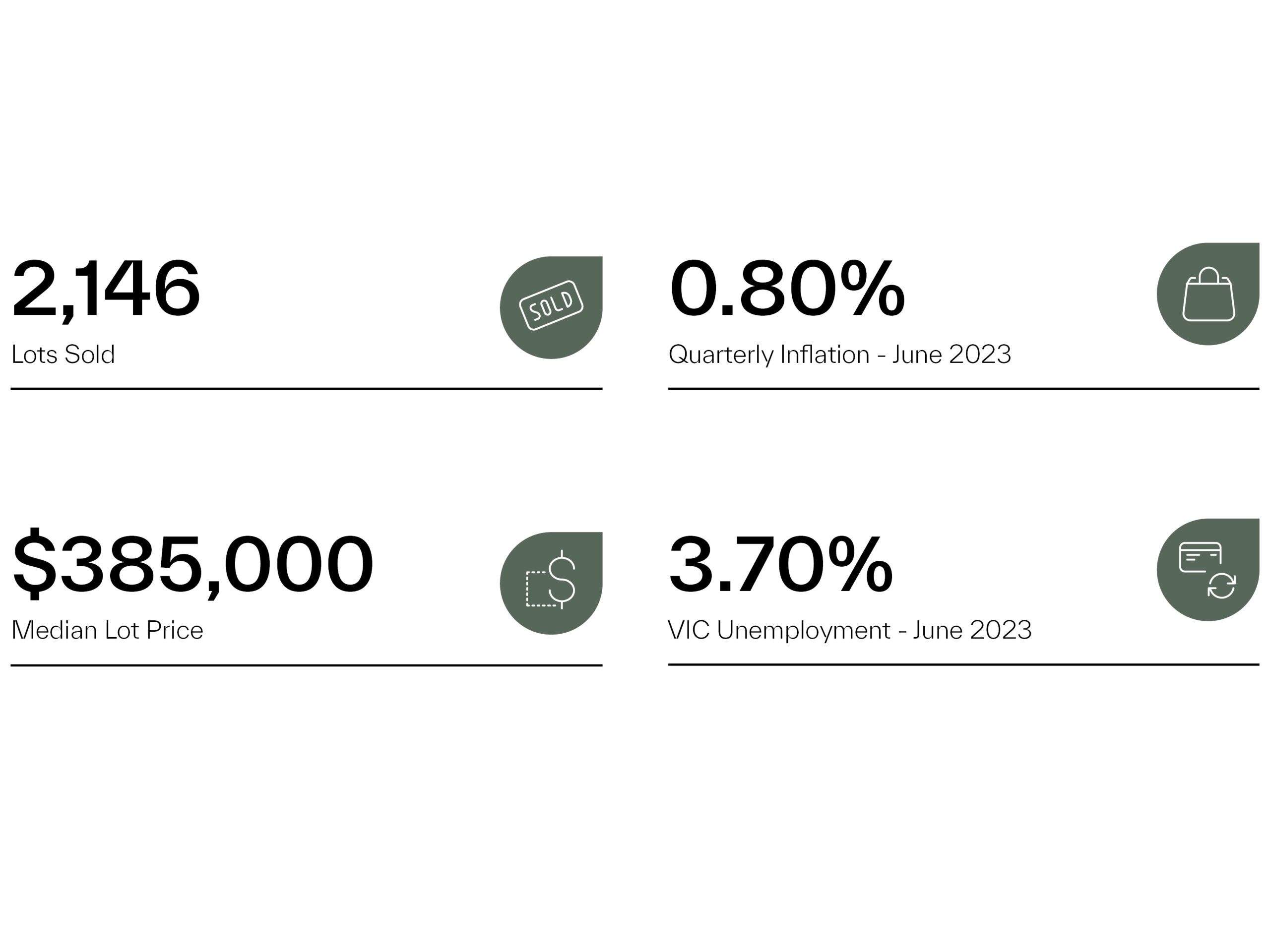

While the recent increase in gross lot sales is a positive sign, it is important to recognise that the market headwinds remain and may result in fluctuated momentum during the second half of the year.

Although the cash rate remained unchanged in July and August, the Reserve Bank of Australia (RBA) is maintaining a tightening bias that allows for the possibility of one more rate rise. Despite projections for at least one cash rate rise by the end of the year, we must note this is being carefully monitored and approached with caution. The annual Consumer Price Index (CPI) growth of 6% this quarter (although lower than expected) remains significantly higher than the target range of 2% to 3%. This is leading many to ask whether the market indeed needs further rate rises or if we will see inflation come down without interference.

Our latest Greenfield Market Report shows that the tight labour market with unemployment rates below 4% is exerting upward pressure on wages, including the residential construction industry. This, coupled with elevated construction costs, will likely keep building a new home an expensive undertaking for many Australians. While overall construction costs remain elevated, building material costs are stabilising.

Amidst this scenario, the new home market faces competition from the established home market, where price corrections offer affordable and comparable housing choices without heightened construction costs. Additionally, an increase in vacant lots on the resale market has intensified competition, with resale lots generally offering lower price per square metre rates than those within estates.

As we look ahead to the second half of 2023, developer incentives and rebates will remain an influential factor in driving lot sales; enabling some buyers to overcome affordability challenges and barriers to entry in the new home market.

This article references findings from our Q2 2023 Greenfield Market Report.