Geelong becomes more expensive than Melbourne

Melbourne’s median lot price contracted by 3.1% over July to $370,000, which was the largest monthly correction in three years since the middle of 2019. Downward pressure is being applied on lot prices from intertest rate rises and steep growth in construction costs. Furthermore, weakening competition among purchasers for vacant lots is also providing buyers with more opportunities to reduce their lot spend without sacrificing lot size, as highlighted by the median lot size remaining steady at 350sqm. Consequently, Melbourne’s median per sqm lot price experienced a similar decline, and more significantly for the first time, became more affordable than the corresponding figure for Geelong. This occurred after Geelong’s median lot size diminished by a sizeable 12.5% to 350sqm, a record low and the same size as in Melbourne, whilst the fall in its median lot prices was more moderate 2% fall to $379,000.

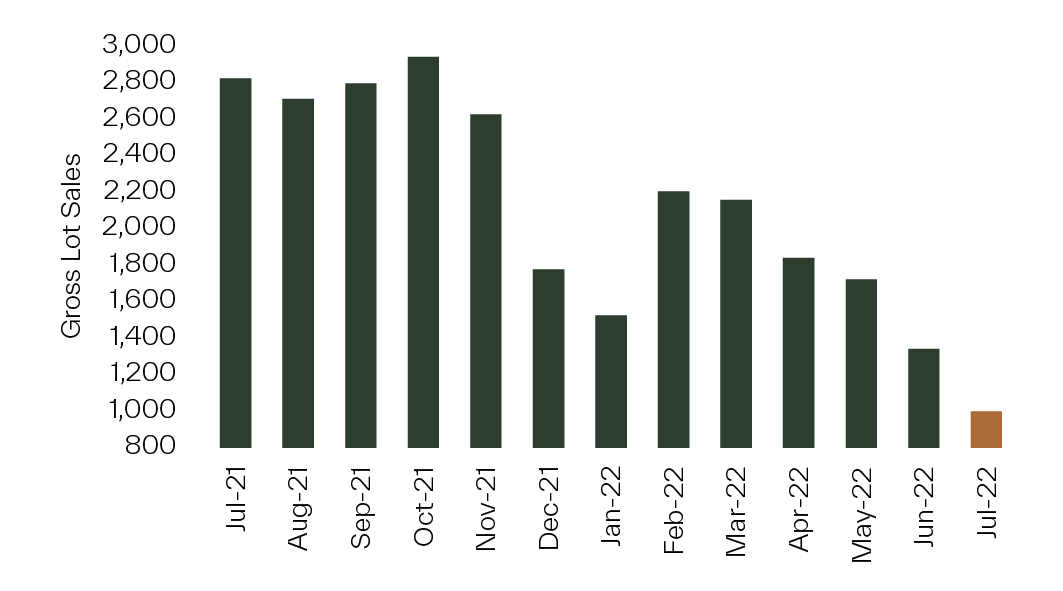

Purchaser sentiment continues to weaken

Successive interest rate rises and strong inflation growth is exacerbating the current cyclical downturn in new home demand with Melbourne, Geelong, Ballarat, Bendigo and Macedon recording 1,000 gross lot sales, a 25% month to month reduction. Compared to the same month in 2021, total gross lot sales are now two-thirds lower with this reduction uniform across all growth areas, except Bendigo.

Northern corridor's proportion of sales falls

The 17% monthly decline in gross lot sales in the South East corridor was nearly half the corresponding figure for the Northern corridor of 33%. Subsequently, the proportion of total sales activity in the Northern corridor fell below one quarter for the first time since February, while the South East corridor’s 20% share was its highest since the same month. Although remaining relatively low, Geelong accounted for an improved 7% of gross lot sales, which was opposite to the small decline in sales activity in Ballarat and Bendigo.

Change in population by age - 2016-2021 Census

Between the 2016 and 2021 Census, persons aged from 0 to 24 years old and 35 to 54 years old accounted for 70% of population growth in the Western corridor, and 60% in both the Northern and South East corridors. With persons aged between 25 to 34 years constituting a further 15% to 20% of population growth across the three growth areas, it emphasises the significance of family households on new home demand. In regional growth areas, the highest concentration of population growth was in the 55 to 74 years age cohort, reflecting the ‘sea-change’ or ‘tree-change’ movement of empty nester and retiree households. Nevertheless, family households remain an important driver of new home demand in regional growth areas.