From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

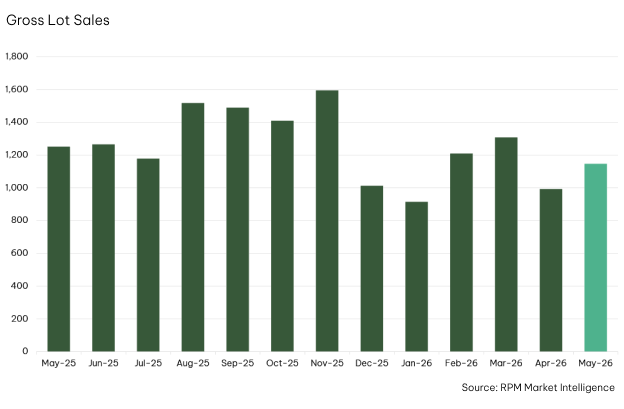

However, the uplift was likely influenced by May containing five trading weekends, along with seasonal factors that suppressed activity in the previous month. While property markets also contended with negative sentiment following taxation changes affecting property investment in FY26/27 Federal Budget, the impact was largely confined to established dwellings, with incentives for investment in new dwellings remaining unchanged.

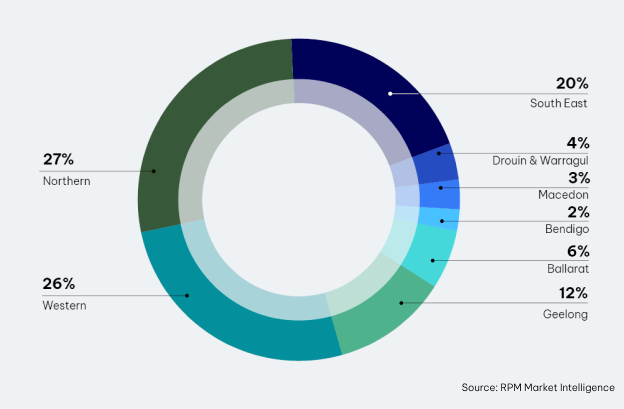

Regional corridors were more subdued, with proportions holding steady month on month. Geelong remained the strongest at 12% of total sales, ahead of Ballarat at 6%.

*Outside of the December-January period.

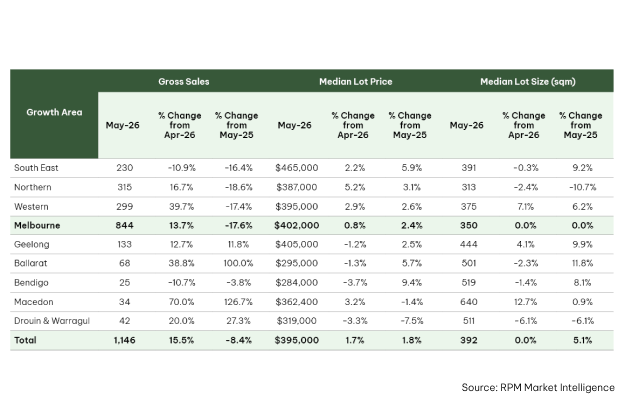

Melbourne’s median lot price increased 1% in May to $402,000, while the median lot size remained stable at 350sqm. Median lot sizes in Geelong continued to expand, growing by 4% to its largest size in over two years at 444sqm. Although, this has not influenced lot prices, with the median contracting by 1.2% to $405,000.

Affordability challenges have led to more nonfirst home buyers among total owner occupier purchasers. RPM Buyer Surveys show that non first home buyers made up 51% of owner occupier purchasers in 2024/25, up from 41% over the prior decade. Loan commitment data also shows that annual growth in new commitments to non first home buyers ran at 5.5%, ahead of the 4.6% recorded for first home buyers.