From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

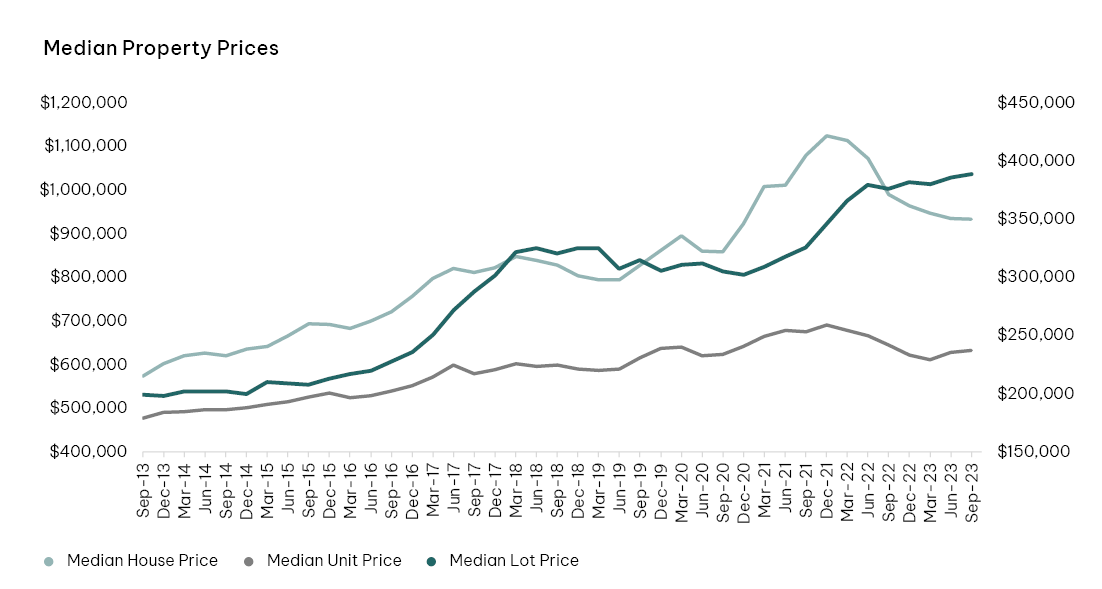

Q3 2023’s interest rate stability (following 12 cash rate increases in the 13 months to June 2023) led to some initial signs of recovery in residential property demand. This was supported by record population growth augmenting the moderate local demand.

In response, vendors were more willing to place their property onto the market; helped by the generally higher-selling spring season. As a result, Q3’s auctions were 24% higher than the same time last year.

Nevertheless, this is only partially offsetting the reduced activity from an increasing number of prospective buyers who are being forced to reevaluate their purchasing decisions (as higher interest rates and subsequent diminished borrowing capacity widens the gap between what they desire in a home to the type of dwelling they can afford). Consequently, many are choosing to delay their property purchase in favour of saving a larger deposit or until market conditions become more favourable, rather than adjusting their home preferences.

As a result, prices are still struggling for momentum, although the annual rate of decline is slowing, and the more affordable unit market has recorded a small uptick on recent prices.

New home demand is weakening after record sales during the 18 months from the start of the HomeBuilder Grant (June 2020). Rising cost of living pressures, higher construction costs, and the potential for more interest rate rises during the first half of 2024 are contributing to cautionary buyer behaviour. Additionally, new supply is being restrained to be commensurate with lower lot absorption to avoid the emergence of a large excess in stock and downward pressure on lot prices.

Subsequently, there has been an increase in rebates and discounts offering 5% to 10% off the headline lot price, with the aim of driving sales activity and absorbing titled and near titled lots that have sat on the market for an extended period.

So, while the headline median lot price in Q3 2023 was at a record level of $389,000 and has escalated by 0.8% from the previous quarter and 3.4% annually, the median lot value is likely to have shown a correction after taking into consideration current buyer incentives.

This article references findings from our Q3 2023 Residential Market and Economic Review.