From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

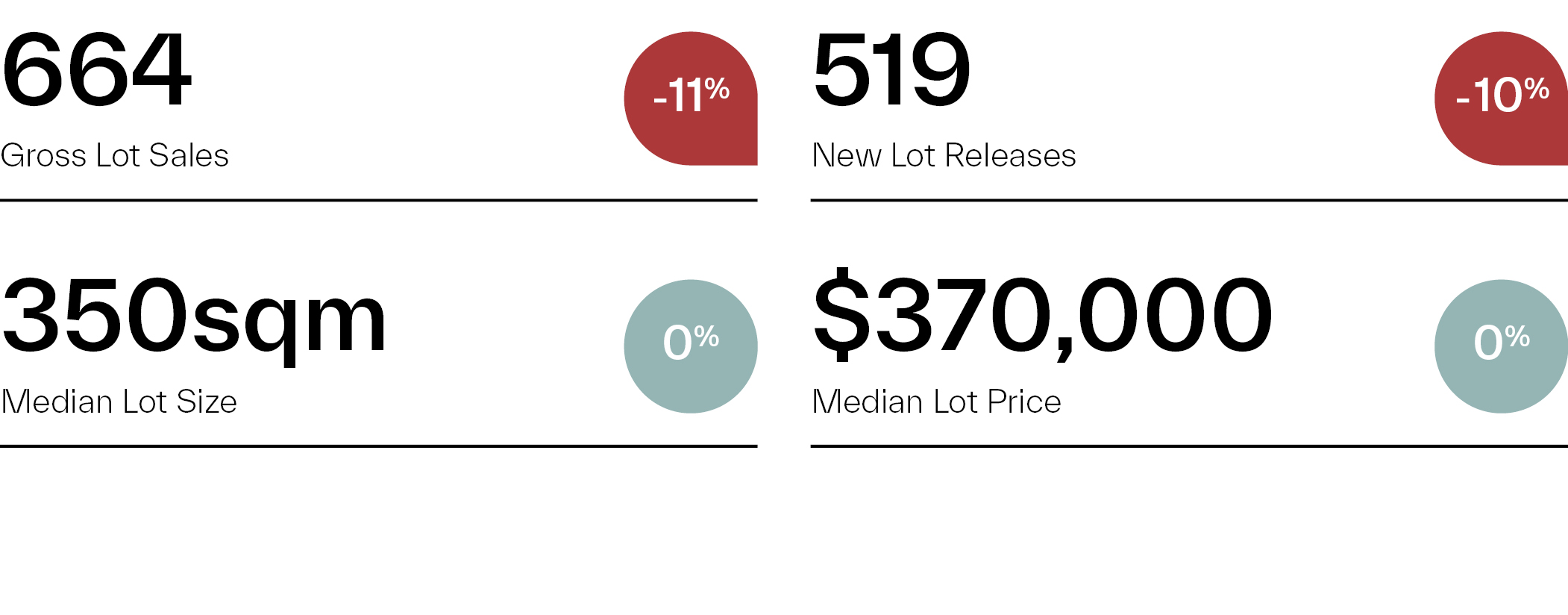

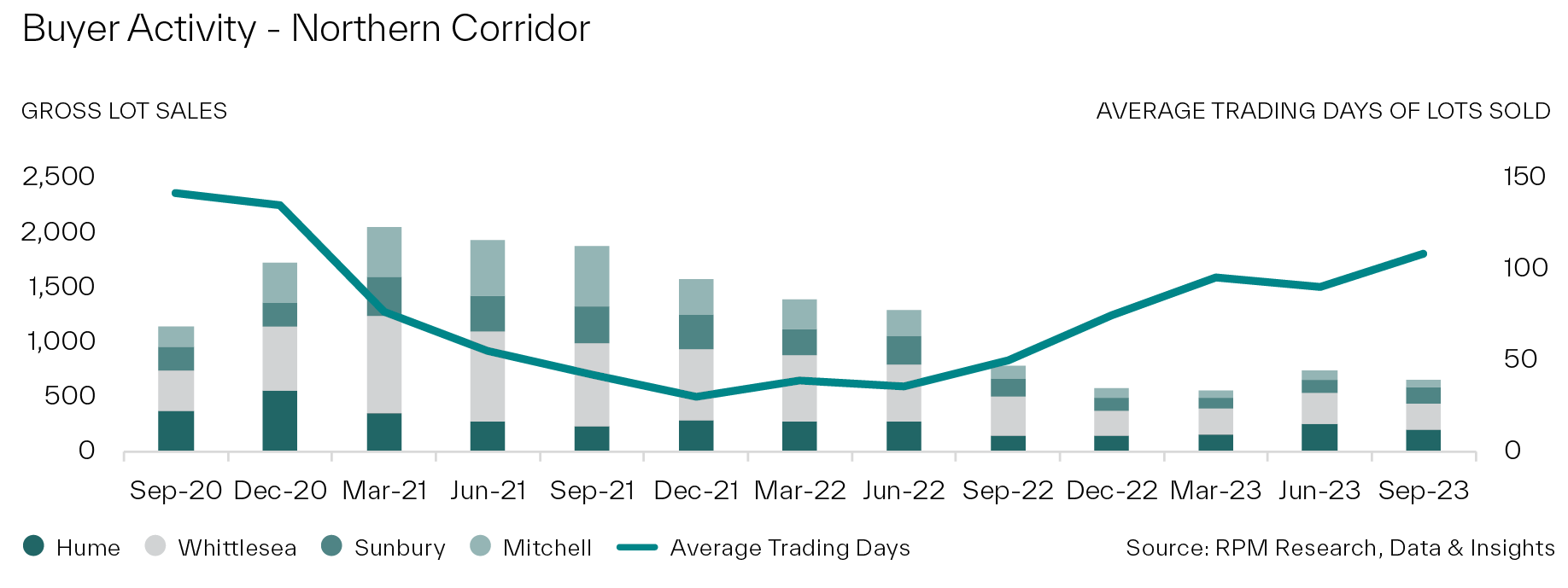

Our Q3 Greenfield Market Report shows the Northern Growth Corridor, which includes Hume and Whittlesea, recorded 664 lot sales over the quarter with sales falling 11% as buyers struggled with reduced borrowing capacity and cost of living challenges.

The 11% decline was almost double that recorded across the broader Melbourne and Geelong growth areas, where sales fell 6% to 2,023 lots. The median lot price in the Northern corridor held steady at $370,000, significantly more affordable than the Western ($385,000), South Eastern ($435,000) and Geelong ($401,100) corridors.

The rate of absorption also continued to outpace new supply, which fell by 10% to 519 new lots, with the North maintaining its record of having the lowest average time on market at 109 days.

RPM National Managing Director of Project Marketing, Luke Kelly, said while sales had fallen, there were positive take-outs from the quarter. “The Northern corridor’s share of total sales across the corridors remains elevated compared to the long-term average and that’s because of its affordability, with the Western and South East Growth corridors 4% and 18% more expensive respectively,” Mr Kelly said.

“Owner occupiers made up a healthy 71% of buyers in the North, with just over half of these first-home buyers. The North also had the lowest average time on market of all corridors at 109 days, which has led to lot absorption continuing to outpace new supply.”

“Developers are also offering 5% to 10% incentives off the headline price of lots which should help spur demand.”

Mr Kelly said it was interesting to see Sunbury had bucked the trend of declining sales within the Northern corridor; “while three of the sub growth areas within the North experienced double digit quarterly declines, sales in Sunbury were up by 21%.”

“Sunbury is becoming increasingly popular due to its position just 40 minutes north of Melbourne’s CBD with buyers also attracted to vineyards, native wildlife, and growing culinary options.”

Our Q3 Greenfield Market Report shows sales across the Melbourne and Geelong growth corridors fell by 58% to 8,129 lots over the 12 months to September 2023. The decline comes after sales rose 13% in the second quarter to 2,146 lots, fuelling hopes of the start of a recovery.

Sales numbers are anticipated to remain suppressed for the near future with the median lot price across the growth corridors up 1% in Q3 to a new record of $389,000. Mr Kelly said quarter two’s gains had fluctuated due to a multitude of challenges facing buyers including affordability, a reduction in borrowing capacity, and the rising cost of living.

“It appears the June quarter may have been an aberration and not a sign of an upward trajectory, although in good news, while sales were down in Q3 compared to the previous quarter they remain above the first quarter of the year,” Mr Kelly said.

“Pressure on demand remains strong, however, due to persistent inflation and the latest increase to the cash rate this month, the market looks like it will remain subdued for some time. Additionally, there is substantial unsold developer stock on market, which continues to grow. This coupled with existing stock from previous buyers selling land they can no longer build on due to difficulties in obtaining finance for construction has kept lot prices in check.”

This article references findings from our Q3 2023 Greenfield Market Report.