From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

Melbourne, along with most capital cities across Australia, currently sits at a weird cusp. Against all expectations and historical data, house prices have skyrocketed through the pandemic.

In the past, a significant shock to the economy has tended to result in falling house prices – in turn affecting the largest source of wealth for households. This has not transpired in the current property market.

While wages have stagnated with the overall uncertainty in the market, house prices have surged by 17.3% over the 12 months to September 2021. A combination of historically low borrowing rates, along with plentiful economic support, has seen Melbourne’s median house prices rise to new heights – reaching $1,010,000 as of the 2021 June quarter.

Additionally, the often criticised apartment market has also reached a new high of $679,500 in June 2021 – marking a significant 9.4% increase over the 12 months.

These record prices raise the question, what should an investor do?

In this article, we uncover four variables that are key to any investment equation.

Firstly, the current economic climate is central. Lockdowns are starting to weigh heavily on both consumer and business sentiment, especially as we lean into the next three months when sales and listings volumes are typically high. More so, buying a dwelling sight-unseen can cause hesitancy as property inspections are currently restricted. For any large property investment, being comfortable with what you are purchasing is paramount.

More buyers and sellers are in the market now compared to 12 months ago. Yet, the strong price growth over this period was largely attributed to a lack of supply on the market, with those in the market to buy eager not to miss out. This created a sense of ‘buy at all costs’ and resulted in remarkable/higher than anticipated price growth. This misalignment in supply and demand is evident in auction levels and clearance rates. Comparing this year to the medium term (over the past two years), Melbourne’s auction market has been considerably active, with a high number of auctions held (peaking in May 2021 with 5,491) and a steadily high clearance rate so far in 2021, with no signs of it slowing.

The latest auction results as of the week ending September 12th has shown there were 151 auctions held, with a staggering 95% clearance rate; this follows on from the previous week with 183 auctions held and a 97% clearance rate. Despite physical property inspections being closed in Melbourne and auctions being held online, Melbourne’s current auction market has maintained its momentum.

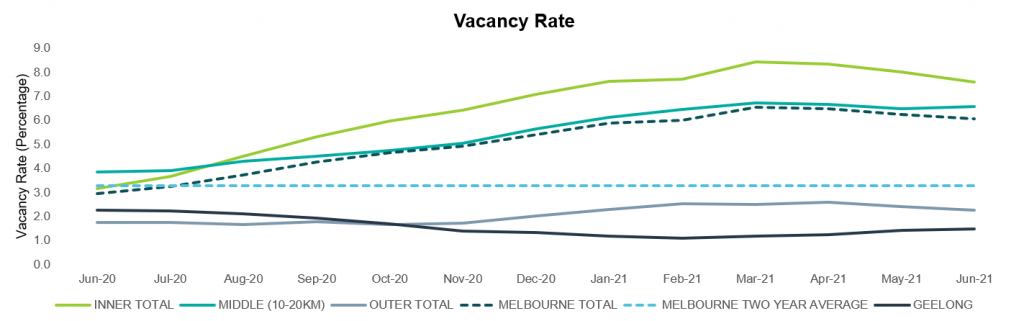

Vacancy rates are at a displeasingly high level in Melbourne at 6.1% – almost double the current two year average of 3.3%. However, we need to look a little deeper into the numbers. The inner and middle-rings see vacancy rates at 7.6% and 6.6%, respectively; this is to be expected, especially in the absence of international demand that largely fill these apartments. Conversely, in the outer ring of Melbourne (or the ‘greenfield’ market) and Geelong, an acute 1.9% are sitting empty.

Vacancy rates drive the direction of rents. With an increased or alleviated vacancy rate, there is limited opportunity to increase rents. In fact, high vacancies often mean discounts and incentives need to be offered for tenants to want to occupy the building. This is the case in the inner ring of Melbourne, but not so in the outer and regional areas, which has seen vacancy rates stay consistently low over the past 12 months.

In a nutshell, it largely depends on your purchase price, ability to manage repayments, and your risk profile regarding vacancy rates. With this, the established house market has shown considerable resilience through the pandemic to a point where it is now out of reach for some to invest in. Conversely, while the apartment market is sitting well below the established house market, it comes with serious concerns around being able to rent it out with the absence of students and closed borders.

This leaves the booming greenfield market! As indicated by tight vacancy rates and growing rents, investors have shifted from buying inner and middle rings to outer rings. With the ability to buy a house and land package for under $500,000, or a townhome for sub $450,000, all investor budgets can be met. RPM’s buyer surveys show that investor activity in the greenfield market has increased from a low of 9% in September 2020 to 33% in June 2021.

The million-dollar question! Well, the answer is quite easy – it comes down to you. Anytime could be the right and equally the wrong time to buy. It solely depends on your own investment goals taking into consideration your budget, risk profile and timeline. These three variables are important now more than ever. If you’re insecure regarding employment or are carrying significant debt, then despite the conducive borrowing environment, this might not be your time to add further debt to the household.

However, if you are secure in your employment and have minimal debt, the ability to borrow money at historically low rates make this a prime time to buy. It is important to remember that property investment should not be a short-term game but a long-term relationship with the market.

This is illustrated in the land market, where you can work through the purchase of land, building a home, and the ongoing rental process for many years to come, while watching the investment appreciate over the long term.

Disclaimer: The commentary provided in this article is the opinion of the team at RPM Real Estate Group and does not constitute financial advice in any way whatsoever. Nothing published above constitutes an investment recommendation, nor should any data or content published be relied upon for any investment activities. RPM Real Estate Group strongly recommends that you perform you own independent research and/or speak with your preferred lending institution.