From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

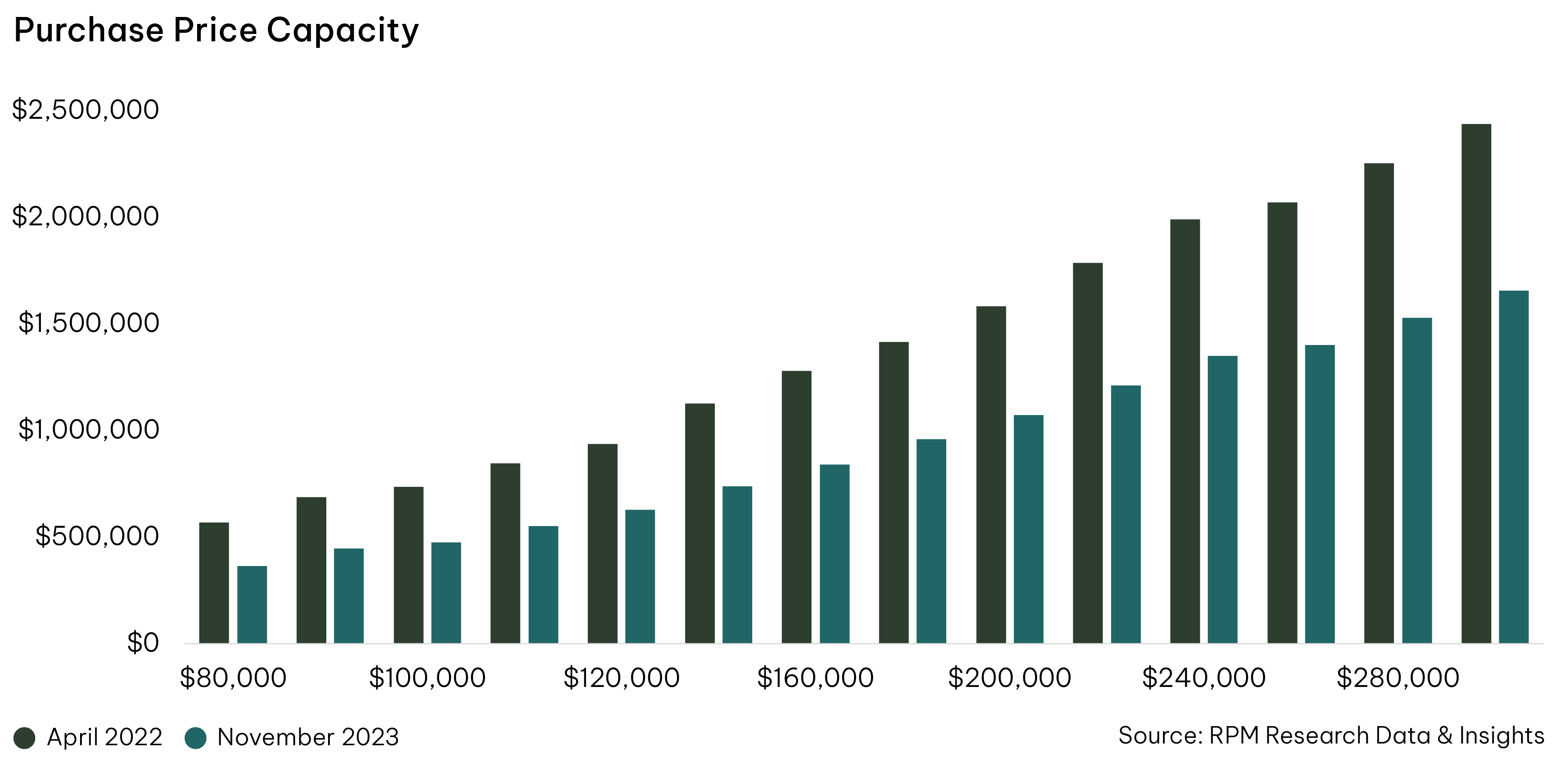

From July to October, interest rate stability hinted at a potential recovery in residential property demand. This was further bolstered by record population growth, supplementing the already moderate local demand. In response, vendors were more willing to list their properties and capitalise on the generally higher selling spring season. As a result, auctions during Q4 2023 were 19% higher than the previous corresponding period.

However, this initial sign of recovery was short-lived – dampened by the 25 basis point rate rise in November. Subsequently, property demand dwindled as prospective buyers grappled with higher interest rates and reduced borrowing capacity, widening the gap between their housing desires and financial realities. Consequently, many opted to postpone their decision to purchase to save up a larger deposit or await more favourable market conditions rather than compromise on their home preferences.

New home demand is weakening after record sales during the 18 months from the start of the HomeBuilder Grant (June 2020). Rising cost of living pressures, higher construction costs, and the rapid 435 basis point rise in the cash rate in a little over one year, are all contributing to cautionary buyer behaviour.

Additionally, developers are restraining new supply to align with lower lot absorption rates, aiming to prevent an oversupply scenario that could drive down lot prices.

Subsequently, there has been a rise in rebates and discounts, offering 5%-10% off the headline lot prices, to stimulate sales activity and clear inventory of lingering titled and near titled lots. While the headline median lot price increased by 1.5% over 2023 to $386,900 in Q4, the actual median lot value likely saw a correction when factoring in current buyer incentives.

This article references findings from our Q4 2023 Economic and Residential Property Market Report.