From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

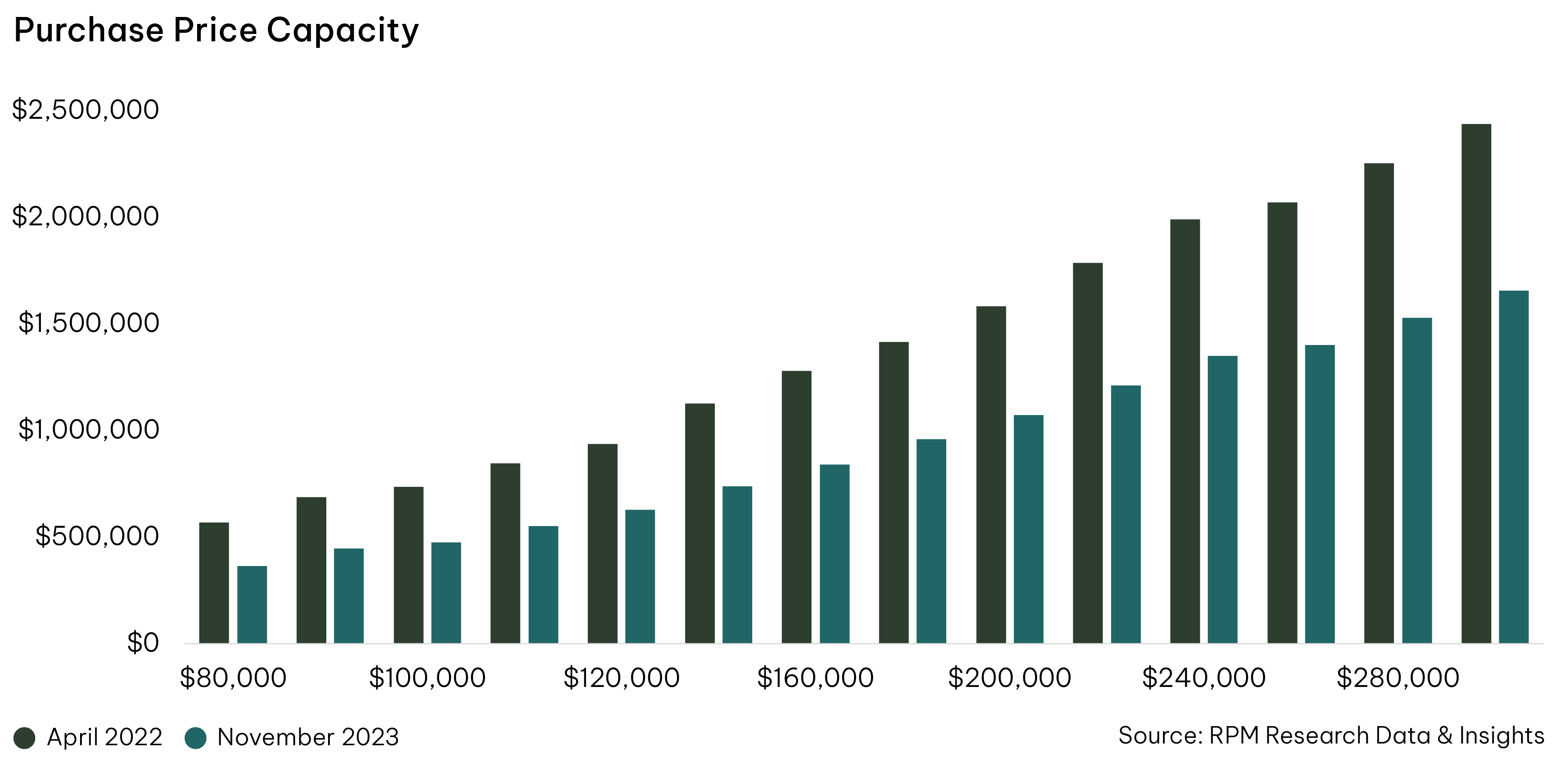

There was a noticeable stabilisation in purchaser sentiment as we entered Q4 2023, aided by the pause in interest rate rises during the four months to October. However, this optimism was short-lived, with confidence shaken by an unexpectedly robust inflation reading in September, leading to the 13th interest rate rise since May 2022 in November.

While this rate rise may have been necessary for other industries, it exacerbated the challenges within the property market marked by diminishing borrowing capacity (which had already declined by around 30% before the last rate rise). The November decision further intensified these challenges, compounding the already significant barriers to entry into the new home market. RPM Buyer Survey results following the HomeBuilder Grant show a shift in buyer demographic. The 35 to 49 age group now constitutes a higher proportion of purchasers compared to those aged 25 to 34 – marking a reversal of previous trends*.

Seasonal impacts deepened this decline in demand with lot sales hitting an 11-year low in both November and December. We also saw this across Melbourne and Geelong growth areas, which fell by 12% (to 1,770 lots) in Q4 2023 compared to the same period in 2022. This was the lowest sales volume for a Q4 period since 2012.

Additionally, the greenfield market faced increased competition from a burgeoning secondary land market with a surge in available re-sale lots where slower absorption rates and heightened stock levels are delaying the entry of new supply; this is seen in a 22% annual decline in releases to 1,452 lots.

The market responded with the continuation of discounts and incentives to support sales activity. These incentives, ranging from 5% to 10% of the headline price, remain crucial in sustaining market momentum. Although lot prices appear stable, the 0.5% decline in Melbourne’s median lot price to $386,900 in Q4 can be attributed to a 1.1% reduction in median lot size to 350sqm, signaling a more significant correction when considering the net price paid by purchasers.

*Over the two and a half years to 2023, 43% of buyers were aged 35 to 54 and 36% of buyers were aged 25 to 34. Over the nine years to FY2021, 33% of buyers were aged 35 to 54 and 47% of buyers were aged 25 to 34.

This article references findings from our Q4 2023 Greenfield Market Report.