From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

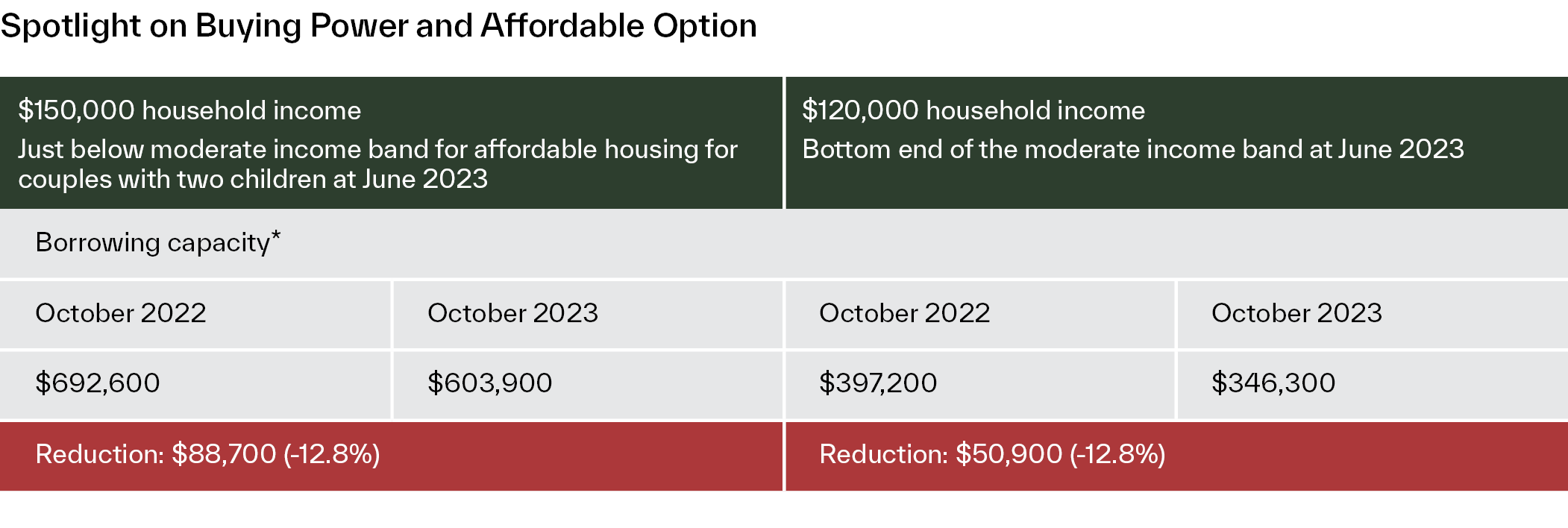

Enquiries show that prospective buyers are still facing significant barriers to entering the new home market. Borrowing capacity remains down by approximately 30% due to the rapid 400 basis point cash rate increase between May 2022 and June 2022. Elevated new home construction costs, initially driven by supply pressures for materials, then labour, have caused a contraction in sales activity following Q2’s pause in decline.

In total, Melbourne and Geelong’s growth areas recorded 2,023 gross lot sales this quarter, a 6% quarterly decrease and a more significant 25% drop from the same time last year. Fragile confidence, coupled with an increasing supply of re-sale vacant lots in the secondary market that is likely absorbing some new home demand, is further contributing to the decline in lot sales activity among estates.

The slower sales rates have extended the average time lots spend on the market to five months. When combined with the rise in returned stock, the total number of unsold lots continues to increase. This is severely hindering the ability to introduce new supply to the market, with only 1,538 lot releases across the growth areas this in Q3. Additionally, upcoming estates are delaying their entry into the market, with only two new estates this quarter.

The greenfield market’s intense competition with the re-sale market and its focus on working through existing stock have led to more rebates and discounts. These incentives typically range from 5% to 10% of the headline price, resulting in Melbourne’s median lot price (without discounts) reaching a new record of $389,000 in Q3, a growth of just under 1% from the last quarter. The price per square metre increased further after the median lot size diminished by 1.3% to 354sqm.

This article references findings from our Q3 2023 Greenfield Market Report.