From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

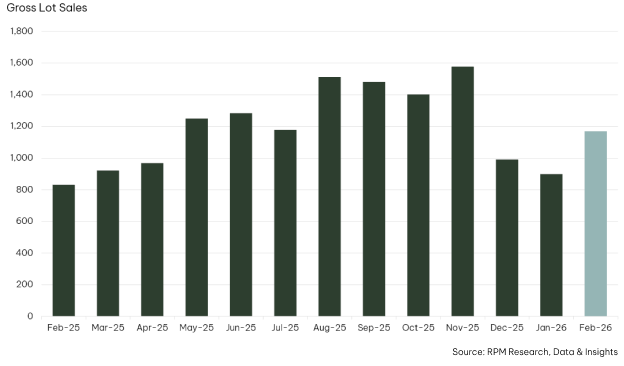

Purchaser sentiment closed 2025 on firmer footing

Purchaser sentiment closed 2025 on firmer footing than a year earlier. Gross sales reached 3,957 lots across metropolitan and regional growth areas in Q4 2025, up 59% on Q4 2024. Activity eased just 5% from Q3, a modest decline given fewer trading days and seasonal sales office closures.

Improved affordability supported the lift in demand

Improved affordability supported the lift in demand. Three interest rate cuts through 2025, combined with wage growth running ahead of inflation for most of the year, restored borrowing capacity. End of year developer campaigns added momentum, particularly for buyers ready to enter the new home market.

Titled stock and new stage releases

Incentives were largely directed toward titled stock, which accounted for 37% of total sales. That share has trended lower across 2025 and was just 30% in Melbourne’s growth areas. With titled supply tightening, developers responded by bringing forward new stages. Melbourne recorded 2,444 lot releases in Q4, steady on the prior quarter and 65% higher year on year.

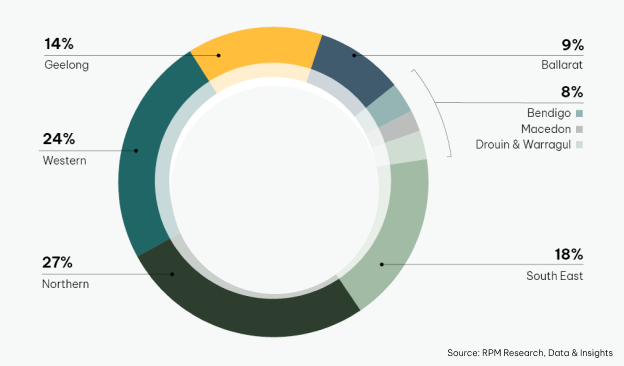

Regional markets lean on existing stock

In the regional markets, titled lots made up 61% of sales, with the strongest concentration in Geelong and Ballarat. The heavier reliance on existing titled stock has slowed new stage releases. Only 424 lots were released across regional growth areas in Q4, still 5% below the same period from the previous year.

Time on market reaches two-year low

In Melbourne, a greater share of recently released, untitled stock sold during the quarter. Average time on market improved to 140 days, the shortest result in two years. Regional markets remains slower, with selling periods extending in the last 12 months.

Smaller formats gaining traction

Product mix continues to adjust. Smaller formats are gaining traction. Townhomes and small lot housing code products were prominent in Melbourne, while regional buyers favoured conventional lots between 300-450sqm. Melbourne’s median lot size eased 1% to 350sqm. The median price also declined 1% to $395,000, holding just below $400,000 for the sixth consecutive quarter.

This article references findings from our Q4 2025 Victorian Greenfield Market Update.